Returning home from my third NRF Big Show 2017, I feel a sense of urgency for continued evolution (rather than revolution…) for retailers to drive better and sounder offerings to us as consumers.

Someone stated (I believe it was RSR Research) that one need to adhere to the continued drive for customer experience, using all means of differentiation rather than sticking to price decreasing, high volume non-differentiated promotions that are brushed off as non-relevant. A winning future retail experience is always personalized, authentic and relevant and if not, all you provide is a commodity offering that can only win on price and that’s when scale comes into play (aka Amazon and Alibaba).

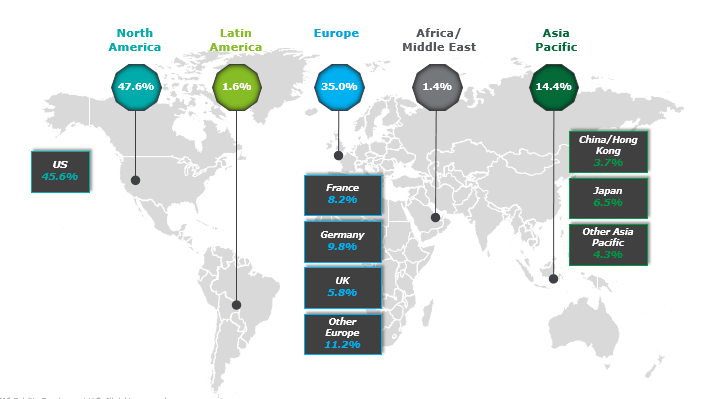

In accordance with a Deloitte analysis, the 250 largest retailers in the world are divided into the following geographies: the US is still in the absolute lead with Walmart as the ‘King of Retail’ followed by Europe and Asia-Pacific with the ever-growing middle-class gaining in size and purchasing power.

Grocery chains are still driving the volumes of the industry at large, with some 67% of the overall generated revenue, according to Deloitte’s report, Global Powers of Retailing 2017. An interesting observation that I made at the Big Show was that the technology partners providing services primarily cover requirements of this segment and they were largely represented in the expo hall.

Research from Kantar reports that the “consumers appear to favor service and experience over merchandise indicating that by 2020, consumers will be spending $2 on services for every $1 spent on ‘stuff’.” This means a definitive increase in what other sectors refer to as the ‘servitization’ of the industry in its focus to finding the ‘ultimate customer experience’, which at least for me was one of the key learnings from NRF 2017.

3 Key takeaways from NRF 2017

1. The customer experience – unique by nature and not a one-size fits all

The industry fumbles – we see some good examples, tests are carried out to better understand the consumers, some non-relevant and some successfully driving growth and better margins. My conviction after the event, however, is that more than ever, this is an evolution and the journey has just begun. Following the trails of the suggested ‘store tour’ in New York, I am certain that the experience examples that were given by NRF mirror the political agenda of NRF as the lobbying organization for American retail more than anything else. Most of the examples were irrelevant at large, and maybe the statement from Deloitte’s Global Powers of Retailing 2017 is really the essence of things:

In these times of political turmoil and digital disruption, I hope it is and I hope that we will see better examples of great customer experiences in 2017. One thing is for sure, this is a continuous evolution for most, if not all, retailers.

2. The merging of the physical and digital world is here to stay

Channel agnostic commerce is here to stay, driving a massive closing of traditional merchant stores, but also giving birth to new concepts and retailers that will influence our industry moving forward. Innovative technologies are emerging to support the merging of the physical and digital world including the Internet of Things (IoT), artificial intelligence (AI), augmented reality (AR) / virtual reality (VR) or even 3D printing – examples were given in the event’s innovation lab.

As a consequence of modern technology – cloud technology, mobility, big data and consequently ‘deep learning’ – the much needed seamless experience across a plethora of customer journeys need to be facilitated, and most IT vendors will stop talking about omni-channel within the near future as this is a prerequisite of today.

The surprise from last year, and to some extent this year, is that some of the largest IT vendors in the world are focusing on building the complete commerce platform, including everything needed to drive a modern retail of the 21st century. More closed rooms and a more gated community setting played a role at this year’s event, and I am not sure it will benefit us as consumers or the retail industry at large. Read more about IDC’s 3rd platform.

3. Transparency

Another tendency this year was the discussion of the consumer demand for transparency. Both in terms of interacting with the retailers – understanding the flow of goods and being able to follow it to a greater extent, but also transparency from a product/service perspective so that we as consumers get full insight into the production of the goods sold.

This will hopefully mean that RFID becomes a reality, and the good examples given on the ROI for these types of investments are really starting to show, too. Examples of retailers taking customization to the next level were also given in terms of Shoes of Prey (customized women’s shoes) and Indochino (customized men’s suits), which have enabled them to scale their business into new countries, offering new products.

Many of us believe that we will see an increased ease with which a customized, more authentic and personal experience can be offered across the industry moving forward in 2017. I also expect that the transparency trend will enable you to track and measure your environmental footprint. Visit our sustainability web page to read more on this topic.

If you found this summary of NRF’s Big Show 2017 interesting, please read my previous blog, “Retail Predications for 2017.”

Do you have questions or comments?

We’d love to hear them so please leave us a message below.